We believe the Agentic Commerce Protocol is about mining the long tail of e-commerce. If you're not careful, you could sleepwalk into a trap that follows a playbook we've seen before. Starting with promises of opportunity and ending with platform consolidation at the potential expense of independent operators.

But before we share our analysis, you need to understand what ACP is and what it enables.

What ACP Actually Is: The Technical Foundation

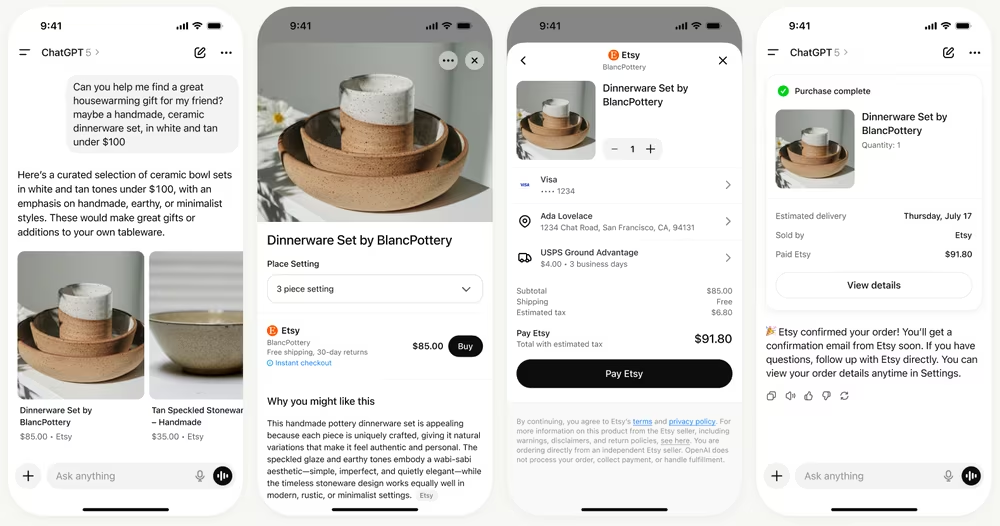

The Agentic Commerce Protocol enables AI agents such as ChatGPT, Perplexity, and Gemini to complete purchases on your behalf without ever leaving the chat interface. Co-developed by OpenAI and Stripe, it's positioned as an "open standard" under Apache 2.0 licensing.

In practice you would go into your AI, ChatGPT for, now as it only works there an go "Find me a christmas present," or a better example as I belive commodity buys will lead the way "A pack of 4 GU10 LED bulbs", only because I bought some, the AI then searches across connected merchants, displays 3-5 products with a "Buy" button, and the purchase completes within the chat: no redirects, no browsing multiple sites, no traditional checkout flow.

There are three parts to making this work.

1) The ACP (Agentic Commerce Protocol) effectively does what you would do when checking out a basket.

2) A2A (Agent to Agent Protocol), in essence, does the bargaining and communication to get the price, etc.

3) AP2 (Agents Payments Protocol) spends your money for you and settles all payments to agents and sellers.

Currently live implementations include ChatGPT Instant Checkout with Etsy sellers in the US, with Shopify integration launching Q4 2025. Etsy sellers are automatically enrolled if they've opted into offsite ads. So there is zero technical work required.

Where is all of this going

So here again we can see how this could play out. And it reminds me of a conference I went to where people were talking about smart devices and washing machines ordering their own detergent and so on. I'll use this use case as an example of what could happen here.

Once all of these three protocols are somewhat ubiquitous, you can genuinely see this happening. Let's take the fridge example. Your smart fridge would have scales, a bit like you have on checkouts, and it would know you're running low on onions.

And you would set a date for your weekly shop, and it would then go and find and negotiate prices and bundle everything together. And you could see a world where groceries would arrive – your onions are from Aldi, your pasta is from Sainsbury's, and the chicken comes from Tesco's, and so on.

All driving down prices.

And then that shop would then send information back to the various merchants and they can then do with that what they want in terms of adjusting pricing and so on.

The vision removes humans entirely from the purchase decision process. The customer becomes an algorithm acting on predefined preferences rather than a person browsing your shop. As one marketplace analyst put it, sellers' "customers" may increasingly be algorithms rather than humans making conscious choices.

The important realisation here is that it fundamentally changes the nature of commerce. When AI agents make purchase decisions, they optimise for measurable variables such as price, delivery speed, ratings, and inventory availability. The intangibles that you, as an independent seller, may compete on, for example, brand story, charitable mission, customer service, and product curation, all become invisible to the algorithm.

Why This Should Concern Independent Sellers

Understanding what ACP is doesn't tell you whether you should adopt it. That requires looking at who actually benefits from this infrastructure and what happens to independent operators when platforms control the transaction layer. I would encourage you to watch this video which shows ACP in action.

The Long Tail Extraction Play

The economic reality for small independent sellers is stark. Despite a 1,200% increase in ChatGPT traffic to e-commerce sites from mid-2024 to early 2025, the absolute volumes tell a different story: ChatGPT contributes "well under 1% of sessions" even at major retailers. This is just the start of agentic commerce and has echos of the past when online sales were negligible.

For independent sellers competing against Walmart, Target, and established platforms, actual traffic resulting from agentic "eyeballs" could be measured in single-digit monthly visits. Because this is unlike SEO and traditional e-commerce, where you can influence visibility, this is much more of a network play - more on that later.

The display mechanics make this worse. Unlike traditional search engines, which show dozens of results, ChatGPT typically shows only 3-5 products per query. There's no pagination, no "see more results." If your product isn't in that initial handful, you don't exist for that purchase journey. What we have here is an exceptionally high-stakes, winner-take-all dynamic.

If we think about it, if only five products show, how do you access this limited visibility – you don't even know, that's like a mysterious black box.

And OpenAI currently states that Instant Checkout "is currently available to approved partners", so in fact, it's a closed system at the moment, despite all the noise about it being open.

The real play is for OpenAI to open up its interface so you can sell on it, but they will be the gatekeepers. To a degree, you can understand it. If I want to own the experience, I don't want rubbish products on my system. But you still will not have an idea of how to improve your products' visibility.

Early signs are that OpenAI will prefer brands and large networks. So if you're an independent seller, how do you do that?

The larger networks, what it looks like at the minute, like Shopify and Etsy, are negotiating direct partnerships, and they're negotiating for their own benefit. Again, there's no disclosure on what terms. And if you're using Shopify or Etsy, and you want access to this channel, you need to accept that negotiated partnership. You can only trust in the fact that Shopify and Etsy have negotiated a favourable partnership because they can come from a position of network strength, and trust that those terms will also benefit you.

We searched extensively for documented case studies of independent sellers—those with revenue under £500K, not on major platforms—who have implemented ACP with published results. We found none. All published examples reference Etsy sellers (automatic integration), pending Shopify merchants, or major brands like Glossier and SKIMS, who disclosed no performance data.

The traffic that does arrive converts exceptionally well; it seems ChatGPT sessions convert at approximately 15.9% compared to 1.8% for Google organic. But high conversion on negligible volume is a false positive. It's like celebrating a 50% conversion rate on two visitors.

The FBA Playbook Returns

The end goal I predict for Algorithmic Commerce Protocol play is not innovation; it is a pattern we've seen before.

Amazon's Fulfilment by Amazon launched in 2006 as "a convenience that made it easier for sellers to manage their logistics". Truly optional, genuinely helpful. By 2015, it had become "almost mandatory to have significant success on the platform", with 82% of top sellers using FBA.

The inflexion point came when Amazon's Buy Box algorithm began favouring FBA sellers. As industry analyst Jason Goldberg observed: "It became increasingly apparent that the only way to win the Buy Box was to be eligible for Prime, and the only way for a third-party seller to be eligible for Prime was to use FBA."

When all is said and done, this is not intrinsically bad if the platform and networks are good stewards for all actors in the game.

There are lessons about the effect of what is effectively monopolistic behaviour. One of them comes from Google Shopping – the EU imposed a €2.42 billion fine in 2017 for abusing its dominant position, displaying its own shopping service over rivals. That was upheld by the European Court of Justice in 2024, and the German court ordered another fine in damages for systemically steering traffic.

It is something that all networks, if you look at it from their position, in a way want to do, because they effectively have their own shareholders and are interested in their own profit. So steering things towards things that they make themselves or other sell channels that they control, and giving those preferential treatment, is always likely to happen.

That is the relationship you're entering into when you work with networks like this, and the ACP structure will create a network.

A Technical Reality: Who Actually Controls This

I'm concerned that this is all marketed as open. And it is all marketing in my view.

Because OpenAI and Stripe, as it currently stands, maintain de facto control through the protocol stewardship. From what I have seen, there are no plans for a truly independent body like the W3C. With a truly independent steering committee, and that would allow a formal process for merchants to join, have some transparency around voting procedures and protocol changes, and basically be a guardian to the implementation of this protocol being truly open and not having commercial gatekeepers.

At the moment, there are gatekeepers at every layer:

Payment Processing: Stripe's Shared Payment Token is the "first Delegated Payment Spec-compatible implementation" ergo it's currently the only option. Stripe, which has 17.15% global market shareand serves 62% of Fortune 500 companies. While ACP claims to be "processor-agnostic," no alternative payment processors have yet implemented compatibility.

For merchants using Adyen, Braintree, or PayPal, the choice is binary: add Stripe specifically for agentic commerce, or build a custom Delegated Payment Spec integration that can take weeks to months to develop.

Platform Access: At the first level, partner platforms like Shopify and Etsy have automatic eligibility. For Stripe merchants, the integration is simplified; however, you still need to apply for approval. And finally, independent merchants using other processors will face potentially complex integration and uncertainty about approval, unless things change.

AI Agent Access: Even after technical implementation, merchants need OpenAI approval to appear in ChatGPT Instant Checkout. This isn't automatic—it's a permission system controlled by gatekeepers, where OpenAI determines eligibility.

The "open" framing obscures the reality that OpenAI and Stripe control who participates, under what terms, and how the protocol evolves. Independent sellers are protocol users, not protocol governors.

The Customer Relationship Myth

Marketing materials emphasise that sellers retain the customer relationship. The technical reality contradicts this claim.

When a purchase occurs through an AI agent, the agent is your customer—not the human who asked for a product recommendation. The platform captures browsing data, purchase intent, comparison behaviour, and preference patterns. You receive transaction-level data: what was ordered, where to ship it, and payment confirmation.

The human buyer doesn't necessarily know they purchased from you, versus the AI simply finding you. They asked ChatGPT for a recommendation, clicked "Buy," and received a product. The relationship lives between the user and the AI platform, not between the user and your shop. And because this is all automated, you can't get the buyer to opt in to your marketing emails.

This mirrors Amazon's long-standing dynamic, in which sellers trade "customers for access." You gain distribution reach but lose the ability to build direct relationships, capture email addresses, or communicate with buyers outside the platform's controlled channels.

Historically, we have seen what happens when these markets play out. You see this again in the example of Fulfilled by Amazon businesses, where aggregators have raised over $12 billion since 2020 to acquire them. They are in effect acquiring predictable, scalable companies.

That reality started with "we are going to make it convenient for you to fulfil your products," and now you may be an acquisition target for aggregators who will become super FBA businesses.

Now, if you get a good price for your business, why not? But if you are a new business entering that world, the barriers start to increase again.

My prediction is that similar things will happen, perhaps not immediately but in the fullness of time, as the ACP networks unfold.

When platforms control customer relationships, they also control the data that informs product development, marketing strategy, and competitive positioning. You're operating with asymmetric information—the platform sees patterns across millions of transactions, whilst you see only your own sales.

The Margin Squeeze: Race to the Bottom

AI agents optimise for measurable variables. Price sits at the top of that list.

Research confirms that AI agents favour lower-priced sellers when products are comparable for commodity products like my LED light bulb example, with known specifications and minimal differentiation. Agentic commerce will literally drive prices down to the lowest available option.

From a consumer perspective, buying light bulbs or batteries this is excellent. For sellers trying to differentiate on service, bundling, or added value, the algorithm doesn't care. If you charge £12 for a product whilst a competitor charges £10, and the specifications match, the AI agent shows the £10 option.

The fee structure compounds this margin pressure. A £100 transaction through ACP costs approximately:

- Stripe: 2.9% + £0.30 = £3.20

- OpenAI: Estimated 0.5-2% (undisclosed) = £0.50-£2.00

- Total: £3.70-£5.20 (3.7%-5.2%)

Compare this to traditional e-commerce at roughly £3.10 (3.1%) or Amazon's 8-15% referral fees. ACP sits between traditional and marketplace economics, but the OpenAI fee remains deliberately undisclosed. The company states merchants pay a "small fee on completed purchases", but refuses to publish specifics. Industry estimates range from 0.5% to 2%, with Sam Altman suggesting a "2% affiliate fee" model in public comments.

Committing to a payment structure where the largest fee component remains undisclosed is financially reckless. Yet this is what independent sellers are being asked to accept.

The £500K Reality Check: Why the Numbers Don't Work

For an independent seller generating £500K annual revenue, the value proposition doesn't add up.

Implementation Costs: Custom platforms require £2,000-5,000+ in development work. WooCommerce basic integration might cost £1,000-2,500 with mid-level developer assistance. This assumes your payment processor is already Stripe—if not, add migration costs.

Traffic Reality: Even major retailers see well under 1% of sessions from ChatGPT. For small independents competing against Walmart and Target in the 3-5 product display window, monthly traffic could be single digits.

No Visibility Control: The ranking algorithm is proprietary and undisclosed. OpenAI states results are "organic and unsponsored, ranked purely on relevance" with no paid placement currently available. But observed patterns show that ChatGPT prefers trusted major outlets over unknown independent shops.https://www.youtube.com/watch?v=-a964k0J9zI

Algorithmic Black Box: Multiple sources report the same query producing completely different results at different times. OpenAI's internal metric shows ChatGPT locates the desired product only 37% of the time with standard search, improving to 64% with the shopping discovery feature. Over one-third of searches remain unsuccessful even with the enhanced feature.

Unknown Fee Burden: Investing development resources and ongoing transaction fees when the largest cost component remains undisclosed represents poor risk management.

Chasing potentially negligible traffic with £2-5K upfront investment, no visibility guarantee, and unknown long-term fees makes no economic sense for most small sellers.

When It Might Make Sense

This isn't entirely doom—specific scenarios justify ACP engagement.

Etsy Sellers: Zero implementation effort, automatic enrolment if you've opted into offsite ads. You may get an extra sale or two with literally no downside.

Shopify Merchants: When the official integration launches Q4 2025, implementation should be minimal. Monitor results before investing further.

High-Margin Unique Products: If you sell specialised items with limited competition and healthy margins, the fee structure is more tolerable. AI agents selecting from fewer options reduce the risk of winner-take-all outcomes.

Strategic Hedge: Implementing minimum technical requirements—structured data markup, robots.txt configuration, basic API readiness—costs relatively little whilst positioning you for future optionality. These investments deliver value in traditional e-commerce regardless of whether agentic commerce succeeds.

The recommendation is to hedge towards preparation, including putting in structured product feeds, an API-first architecture, and markup for your products – these are, in essence, best practices anyway.

Particularly starting to get a first-party communication with your customers, so doubling down on those will create value even if ACP doesn't hit any meaningful scale.

And again, where I see immediate traction and direction of travel is on commodity products.

Network Effects Compound Quickly

We can be under no illusion about how quickly network effects can play out.

Stripe already controls over 17% of the global payment processing market. The widespread adoption of ChatGPT means OpenAI controls a large share of the AI agent market, and if you're on Shopify or Etsy, they'll control merchant onboarding.

You can see how this is a circle where each partnership strengthens the other's position.

Independent sellers need collective defensive mechanisms, but what those look like remains unclear. When platforms own infrastructure, they accumulate data and relationships that create compounding advantages. Individual sellers, operating independently, cannot match this structural power.

Historically, when platforms control essential infrastructure, they win. Independent sellers need some form of network effect they can control—but honestly, we don't know what that would look like in practice. Collaborative marketplaces that preserve seller ownership? Industry consortia that negotiate collectively? Open-source alternatives governed by merchant committees?

What's clear is that operating entirely independently makes you maximally vulnerable to platform consolidation. The long tail gets mined precisely because each seller acts alone with no collective leverage.

Make No Mistake: This Will Happen

Disruption in e-commerce is a laser focus for gen AI companies, as is advertising revenue. Regardless of how this plays out, you may have little choice but to participate.

So here's what you should do now.

Strengthen Defences AI Agents Cannot Replicate

Owned Audience: Build email and SMS lists you fully control. Consider building these collectively with other sellers in your category. Email marketing remains one of the most profitable acquisition channels with minimal costs and owned subscriber data. SMS shows 45% response rates with 98% open rates.

Expertise Positioning: Create genuinely helpful content—not volume/velocity SEO farming, but peer-level expertise that positions you as a trusted adviser. Content aligned with Google's E-E-A-T principles (Experience, Expertise, Authoritativeness, Trustworthiness) provides sustained long-term value.

Customer Experience: Invest in service levels, flexible returns, loyalty programs, and relationships that AI agents cannot replicate. Human expertise builds deeper loyalty than algorithmic recommendations. Repeat customers spend 67% more than first-time buyers.

Product Differentiation: Curated bundles, customisation, limited editions—things that resist commodity price comparison. High-margin unique products are less vulnerable to algorithmic downward price pressure.

Subscription Models: Ongoing relationships and replenishment services create predictable recurring revenue independent of algorithm changes. Subscriptions build customer intimacy whilst reducing dependence on continuous acquisition marketing.

Local/Community Connection: Compete on values alignment and emotional loyalty—meaning, not just price and convenience. DTC brands with strong community achieve higher customer lifetime value.

Omnichannel Presence: Live events will make a significant comeback as AI erodes online trust. Physical touchpoints matter when digital commerce becomes automated and impersonal. Counter-position against purely algorithmic commerce.

Hedge Strategies That Deliver Value Regardless

Product Information Management: Implement a centralised system maintaining a single source of truth for all product data. This supports traditional multichannel selling whilst preparing for ACP if needed.

API-First Architecture: Migrate from monolithic platforms to headless or composable architectures with exposed APIs. This enables flexible integration with any future channel without rebuilding core systems.

Enhanced Analytics: Build comprehensive tracking that captures granular customer behaviour, product performance, and attribution. This powers traditional optimisation whilst preparing the ACP-required data foundation.

Content Enrichment: High-quality product photography, detailed specifications, size guides, and sustainability information. This improves traditional conversion whilst providing the rich context AI agents need. Brands with enriched product data see 34% higher click-through rates.

Automated Workflows: Document and automate order fulfilment, inventory management, and customer service. Operational efficiency pays immediate dividends in traditional operations whilst preparing for automated order flows enabled by ACP.

The Strategic Posture: Defensive, Not Opportunistic

At this early point, the strategic posture should be defensive, not opportunistic, and you should be ready to shift this as the mechanics evolve and transparency increases.

If you're on Etsy: Click the opt-in button. Zero cost, zero risk, possibly an extra sale or two.

If you're on Shopify: Wait for the official integration (Q4 2025). Monitor but don't rush custom development.

If you're independent: Implement minimum technical steps—structured data, robots.txt, basic API readiness—and monitor carefully.

Participation in time may become mandatory for competitive parity. The adoption is small now, but the forces behind it—Stripe, OpenAI, Etsy, Shopify—are substantial. What's critical now is that independent sellers really up the game on building trust and first-party connections with customers. Whilst always important, this is now critical.

In essence, this thing may happen to you whether you like it or not. But you need to know the likely long-term direction of travel.

Prepare. Prepare. Prepare.

What to Monitor

Track these specific signals, not vendor announcements:

Actual Traffic Metrics: Check your server logs for activity from GPTBot, ChatGPT-User, and OAI-SearchBot. Monitor referral traffic from chatgpt.com in your analytics. Are you actually seeing AI agent visits?

Fee Escalation: Watch for OpenAI commission disclosure and Stripe rate changes. If baseline fees rise above 3-5% within 18 months, the extraction model is accelerating.

Self-Preferencing Patterns: Are large platforms systematically favoured in AI recommendations? Track whether 70%+ of visible results go to platform ecosystem merchants (Amazon FBA, Shopify Plus, enterprise accounts).

Data Asymmetry: Who's using your product data and for what? Watch whether platform-operated brands launch competing products 6-12 months after you achieve category success.

Customer Relationship Control: Can you still reach buyers directly? If 40%+ of revenue flows through channels where you lack customer contact information, you've created dangerous platform dependency.

Warning Thresholds

If these conditions emerge, ACP has consolidated rather than democratised:

- 70%+ of AI recommendations go to merchants in platform ecosystems

- Baseline transaction fees rise above 3-5% within the first 18 months

- 40%+ of revenue through channels where you lack customer data

- Compliance costs exceed £10-25K annually for small merchants

- Must maintain 3+ incompatible implementations to reach mainstream AI agents

When you cross these thresholds, double down on owned channels, direct relationships, and defensible differentiation.

Eyes wide open. Not paranoid, but not naive either.

My analysis draws on extensive research across vendor documentation, industry reports, regulatory filings, and technical specifications. I'm applying 23 years of operating and digitising independent businesses to interpret that evidence. I found no independent sellers with published ACP implementation case studies under £500K. All available evidence comes from platform partners, major brands, vendor marketing materials, and consultant projections. Make of that what you will.